Chiffres clés of l’action NVIDIA

- Current price: 210,69 $

- Target price (average): environ 550 $

- Target market price: environ 300 $

- Potential total return: environ 160 %

- Annualized internal rate of return: approximately 23% per year

- Reaction to the results: -1.77% (May 20, 2026)

- You lose maximale: 20,22 % (30 mars 2026)

Available now: discover the upside potential of your favorite stocks thanks to TIKR’s new valuation model (it’s free) >>>

A company that didn’t need the money just borrowed $25 billion

NVIDIA (NVDA) generates more free cash flow than almost any other company in the world; the question that naturally arose this week was simple: why borrow? The answer is the most revealing thing about this title at the moment. On June 15, NVIDIA launched its largest bond issue to date, amounting to $25 billion, its first issuance since 2021, and the transaction was finalized on June 18. The stock closed that day at $210.69, up 2.95%, close to its all-time high.

It’s not the amount that makes the news, but the demand. The issuance attracted approximately $85 billion in orders, more than three times the size of the deal, which allowed NVIDIA to increase the issue size by $20 billion and reduce its borrowing cost. The bonds are divided into seven tranches maturing until 2056. A 30-year bond is a bet that the development of AI infrastructure will extend over several decades, and is not a simple passing cycle.

This is not a financial rescue. NVIDIA holds more cash than debt, with net debt of -$40 billion even after this fundraising. The company procures long-term, low-cost capital to finance both its growth and shareholder returns, without diluting capital. This is the bullish scenario for this operation. The bearish scenario is the opposite: if demand for AI cools, 30-year debt raised at the height of a capital spending boom risks aging poorly.

The timing matches what management has always said

Two weeks earlier, at the Bank of America Global Technology Conference, CFO Colette Kress explained why NVIDIA needed a broader financial toolkit. She had directly quantified future supply commitments. “We basically have about $124 billion in commitments,†said Colette Kress, executive vice president and chief financial officer. These cash flow needs are guaranteed for years to come, which is exactly what long-term debt is for.

Ms Kress also confirmed the roadmap underlying this request. Vera Rubin, NVIDIA’s upcoming data center platform, is ‘ready for Q3’ and in full production; she estimated that Blackwell and Rubin together represented a potential of around $1 trillion between 2025 and 2027.

Debt also frees up liquidity for a sharply increased return on investment. NVIDIA authorized an $80 billion stock repurchase program on May 18 and significantly increased its dividend. Ms. Kress was blunt about the priority: “The amount we can return to shareholders – 50% or more – is definitely one of our top priorities,” confirming the new dividend at “$1 per share per year.” When asked why it wasn’t 75%, she simply replied: “We’re working on it.” HAS”

View historical and forecast estimates for NVIDIA stock (it’s free!) >>>

The discount that continues to follow NVIDIA

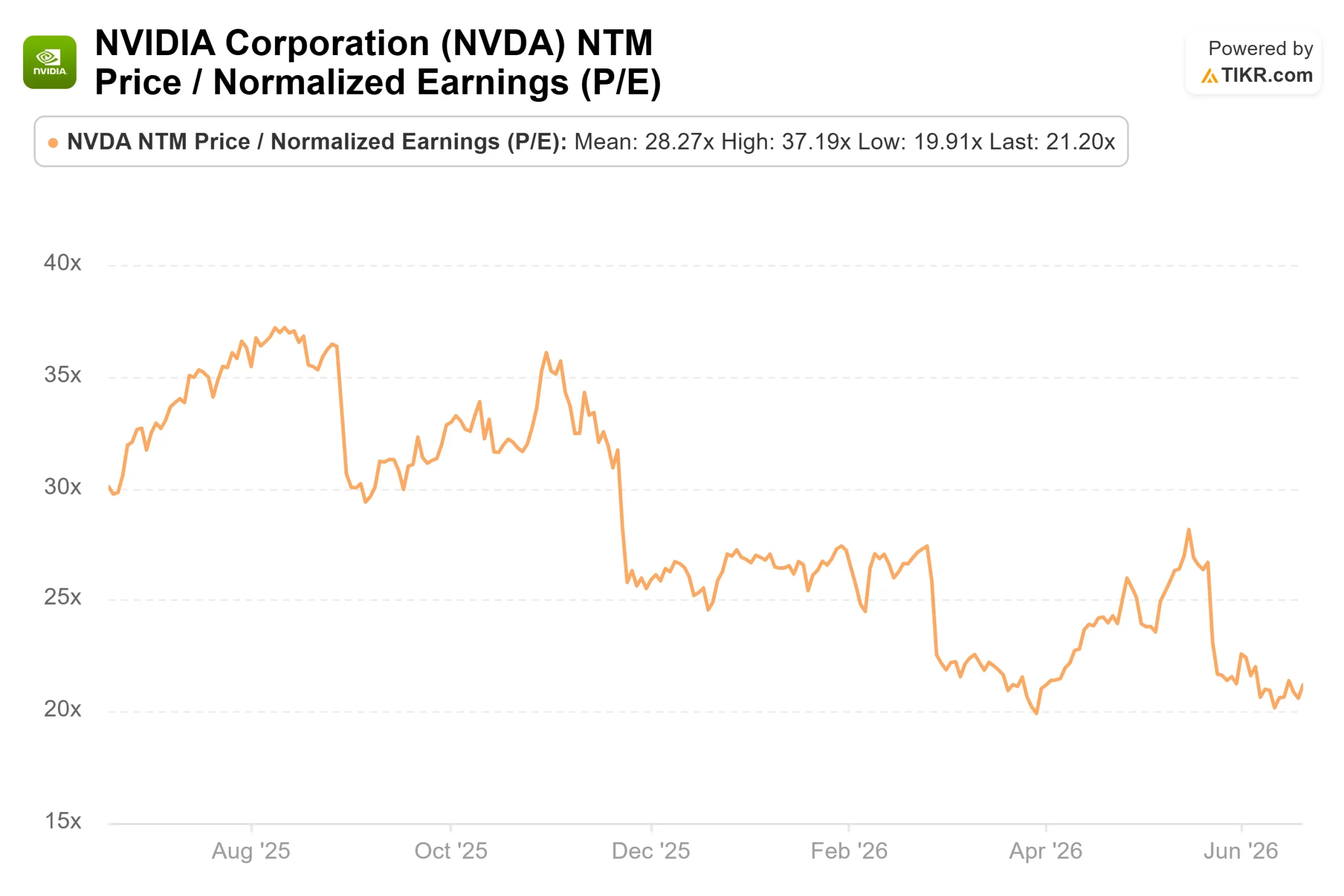

This is where the tension lies. NVIDIA is the most valuable company in the world, with a market capitalization of $5.1 trillion, but it trades at a discount to its competitors on the metric that matters most to a high-growth company. Its price/earnings (P/E) ratio for the next twelve months is 21.20x. Among the semiconductor industry competitors listed on TIKR’s “Competitors” page, Broadcom trades at 26.13x and AMD at 61.63x. The fastest growing company in the group is one of the cheapest.

This gap is not the result of chance. Export controls remain pending, and NVIDIA forecasts zero revenue in China for data center computing solutions. Custom chips from hyperscalers threaten the GPU. And after the release of results on May 20, the stock fell 1.77% even though revenues increased 85% year-over-year to reach $81.6 billion. NVIDIA has a history of posting great numbers while experiencing massive sell-offs, as expectations exceed even strong results.

Fundamentals continue to widen the gap between price and performance. That same quarter generated $48.6 billion in free cash flow, a base that makes taking on $25 billion in new debt seem prudent.

Find out how NVIDIA performs compared to its competitors in TIKR (it’s free!) >>>

Analysis advanced you model TIKR

- Current price: 210 ,69 $

- Target price (average): ~550 $

- Potential total return: ~160 %

- Annualized internal rate of return: ~ 23 % / an

View analyst growth forecasts and price targets for NVIDIA stock (it’s free!) >>>

The model’s entry price corresponds to the real-time closing price, and the target is reached in early 2031. Two revenue drivers underpin this scenario: the rise of the Blackwell and Vera Rubin platforms, and diversification into AI clouds, enterprises and sovereign states, beyond traditional hyperscalers. Driving margins is NVIDIA’s pricing power across its entire product line, with net profit margins estimated at around 55%. The main risk lies in the compression of multiples, because the model already expects a moderate decline in the annual price/earnings (P/E) ratio, and any more marked revaluation would call into question the calculations.

The optimistic scenario: If revenue growth of more than 20% (intermediate scenario) continues, the NVIDIA stock price should approximately double from its current level. The pessimistic scenario: a slump in demand or a shock linked to China would transform these long positions into an example not to be followed, and the multiple would continue to contract.

Conclusion

The next test will be the report for the second quarter of the 2027 financial year, expected at the end of August. Watch data center revenues and prospects in China: a significantly better-than-expected result would confirm that deployment continues to accelerate, and that the $25 billion was well borrowed. A downward revision of forecasts, or a deficit linked to China, would prove the bears right and the discount would be maintained. The bond market has just signaled what long-term investors are thinking. By September, NVIDIA’s income statement will tell if they were right.

Find out which stocks billionaire investors are buying so you can follow the moves of savvy investors with TIKR.

Should you invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data used by professional analysts to answer precisely this question.

Consult NVIDIA and you’ll see several years of historical financial data, Wall Street analysts’ forecasts for revenue and earnings for upcoming quarters, how valuation multiples have changed over time, and whether price targets are trending up or down.

You can create a free watchlist to follow NVIDIA as well as all the other actions that interest you. No credit card required. Just the data you need to form your own opinion.

Analyze NVIDIA for free on TIKR →

Looking for new opportunities?

Warning :

Please note that articles published on TIKR do not constitute investment or financial advice from TIKR or our editorial team, nor recommendations to buy or sell any security. We create our content using TIKR Terminal investment data and analyst estimates. Our analysis may not include the latest company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

{kind=link}