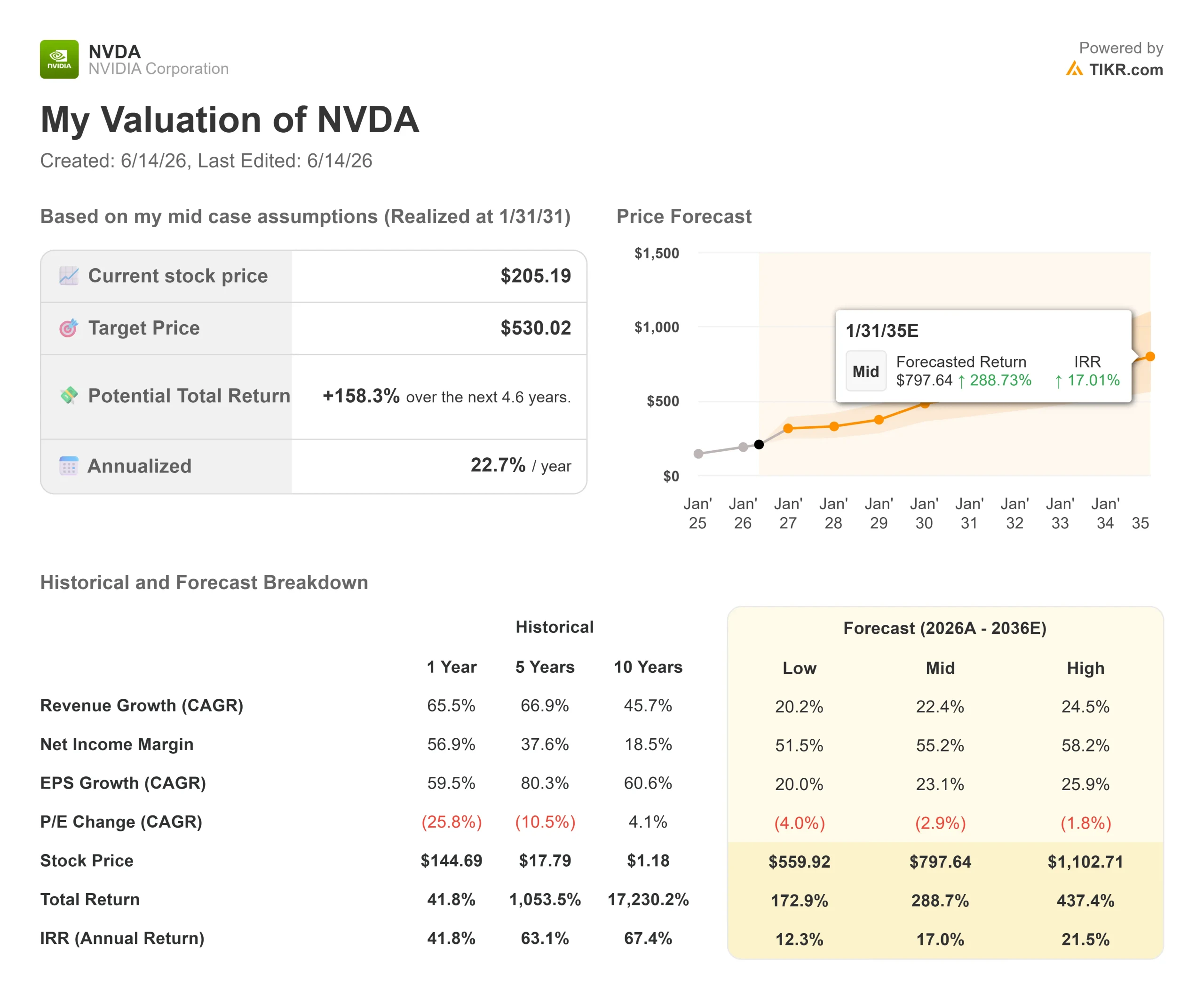

Chiffres clés of l’action NVIDIA

- Current price: $205.19 (closing June 12, 2026)

- Target price (average): ~530 $

- Target market price: ~299 $

- Potential total return: ~ 158 %

- Annualized internal rate of return: ~23 % / an

- Reaction to the results: -5.46% (25 February 2026)

- You lose maximale: -20,22 % (30 mars 2026)

Now available: discover the upside potential of your favorite stocks thanks to TIKR’s new valuation model (it’s free) >>>

What happened?

NVIDIA (NVDA) just did something that a company growing revenue at 85% per year almost never does. Along with its May 20 earnings release, the board increased the quarterly dividend from $0.01 to $0.25 per share, a 25-fold increase, and authorized an additional $80 billion in stock repurchases with no expiration date, according to NVIDIA investor relations filings.

This is where the tension lies. Hypergrowth companies hoard their cash because reinvestment generates a compound return faster than any dividend. Mature companies are redistributing their cash because they are running out of more promising ideas. NVIDIA does both at the same time, and the market doesn’t really know what to think about it. The stock closed at $205.19, about 13% below its 52-week high of $236.54, even as the company posted record results.

The real question is what management tells you when such a fast-growing company starts paying dividends to shareholders.

A record quarter, but the market didn’t pay attention to it

This return on investment is not the result of an economic slowdown. NVIDIA reported revenue of $81.6 billion for the first fiscal quarter of 2027, up 85% from the previous year, with data center revenue of $75.2 billion, up 92%, according to its earnings release. Adjusted EPS of $1.87 exceeded Wall Street’s forecast ($1.77) by 5.54%, continuing an uninterrupted streak of better-than-expected results. Management forecast second-quarter revenue of around $91 billion, above consensus of around $87 billion.

The reaction to the previous quarter speaks volumes. After the report was released on February 25, NVDA fell 5.46% in the following session, despite better-than-expected results. This gap between exceptional operational performance and stagnant action characterizes NVDA’s price. When stocks are priced near perfection, a better-than-expected result is the price to pay.

It is this context that the investment program reflects. NVIDIA generated free cash flow of $96.7 billion in fiscal 2026, and the first quarter alone produced $48.6 billion, nearly double the previous year’s figure. CFO Colette Kress said the company intended to redistribute at least half of that amount to shareholders, presenting the measure as sustainable: “The ability to redistribute 50% or more is absolutely one of our priorities, not just for today, not just for tomorrow, but for the long term. HAS”

View historical and forecast estimates for NVIDIA stock (it’s free!) >>>

Why share buyback is more meaningful than dividend

The yield remains low, at around 0.5%, so income is not the subject. What matters is what the takeover implies in terms of valuation in the eyes of management. The additional $80 billion comes on top of the approximately $38.5 billion already available, giving NVIDIA approximately $118 billion in repurchase power. Companies don’t commit as much to their own stocks unless they think they are worth more than the market gives them credit for.

This confidence is based on a base of demand that has expanded. Kress pointed out that what NVIDIA calls AI Cloud Infrastructure and Enterprises (i.e. newly built AI clouds and national AI factories, rather than repurposed general purpose clouds) is likely the fastest growing part of the data center industry. Faced with the pessimistic argument that custom chips are eroding NVIDIA’s market share, her response focused on the software, not the specifications: a fixed chip “was defined at the time it was designed… She “does not have the capacity to adapt later”, while NVIDIA’s platform evolves with each workload.

Vera Rubin catalyst expected in third quarter

This is not an activity reaching maturity and at the end of the cycle. At GTC Taipei, NVIDIA confirmed that its Vera Rubin platform had entered full production, and Kress clarified the timeline: “It’s coming soon. She’s ready for the third trimester. » This places the start of production in the quarter ending October 2026, earlier than many investors expected. The new Vera processor opens a new product line, built on NVIDIA’s own cores, offering according to management approximately twice the performance of x86 alternatives, and can be sold standalone.

NVIDIA’s premium is lower than its reputation suggests. It trades at 16.43x EV/EBITDA over the next 12 months versus 19.53x for Broadcom, and at 20.65x forward earnings versus 58.68x for AMD. For the fastest growing company in the group, with a current gross margin of 74.1% and a trailing twelve month return on invested capital of 77.2%, the discount to its slower growing peers is more of a relative value than a red flag.

The market followed the fundamentals. The average target rose from $268.61 in April to $298.93 in June, implying approximately 46% upside potential, with 49 Buy recommendations, 10 Outperform, 2 Hold, and just one Sell. The overall risk lies in the compression of multiples: NVDA has the largest market capitalization in the world, and any fluctuation in spending by hyperscalers or a prolonged closure of the Chinese market could quickly lead to a revaluation of its price.

Find out how NVIDIA performs compared to its competitors in TIKR (it’s free!) >>>

Analysis advanced you model TIKR

- Current price: 205,19 $

- Target price (average): ~530 $

- Potential total return: ~158 %

- Annualized internal rate of return: ~23 % / an

View analyst growth forecasts and price targets for NVIDIA stock (it’s free!) >>>

The intermediate TIKR scenario, realized on January 31, 2031, values NVDA at approximately $530, representing a total return of approximately 158% over 4.6 years and an annualized IRR of approximately 23%. The two drivers of the revenue CAGR are continued capital spending by hyperscalers and Vera Rubin’s rise to corporate, sovereign and ACIE customers, supporting a central assumption revenue growth rate of approximately 22%. The margin driver is data center operational leverage, which maintains a net income margin of approximately 55%. The main risk lies in the compression of multiples, because the premium leaves little room for maneuver in the event of disappointment in growth.

Optimistic scenario: demand for agentic computing remains strong and the deployment of Vera Rubin is proceeding as planned, pushing growth and margins up the range. Pessimistic scenario: Hyperscaler spending normalizes, or custom chips gain market share faster than expected, compressing both the multiple and the growth rate.

Conclusion

Watch for data center revenue in NVIDIA’s fiscal second quarter 2027 report, due in late August 2026. Management has projected total revenue of around $91 billion. Achieving that goal, with data center revenue well in excess of the just-reported $75.2 billion, would confirm the demand that Kress called “vertical” and that Vera Rubin is driving. A hiccup, or any sign of slowing orders from hyperscalers, would give the bears their first hard evidence and put the premium at risk. The ROI program tells you what management is thinking. August will tell you if the cash flow that funds it continues to grow.

Find out what stocks billionaire investors are buying so you can follow the moves of savvy investors with TIKR.

Should you invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data used by professional analysts to answer precisely this question.

Consult NVIDIA and you’ll see years of historical financial data, Wall Street analysts’ forecasts for revenue and earnings for upcoming quarters, how valuation multiples have changed over time, and whether price targets are up or down.

You can create a free watchlist to follow NVIDIA as well as all the other actions that interest you. No credit card required. Just the data you need to form your own opinion.

Analyze NVIDIA on TIKR for free →

Looking for new opportunities?

Warning :

Please note that articles published on TIKR do not constitute investment or financial advice from TIKR or our editorial team, nor do they constitute recommendations to buy or sell any stock. We create our content using TIKR Terminal investment data and analyst estimates. Our analysis may not include the latest company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

.jpg "Attention, autres sports : léquipe nationale américaine de football a marqué les esprits pour ses débuts en Coupe du monde, et le football américain pourrait ne plus jamais être le même | Goal.com Français")

{kind=link}